Table of Contents

Compound interest is the closest thing to magic in finance, and almost no one acts like it. Over more than two decades advising Australian families, the single most expensive mistake we see is not a bad stock pick or a poorly timed property purchase. It is waiting. Waiting for the right market, the right balance, the right amount of certainty. The maths of compounding does not reward perfection. It rewards time.

This piece walks through the two-investor case study that makes the point in plain English, then shows what 30 years of Australian asset class returns actually look like, and finishes with what a wealth builder in Australia today should do with the lesson.

The two-investor thought experiment

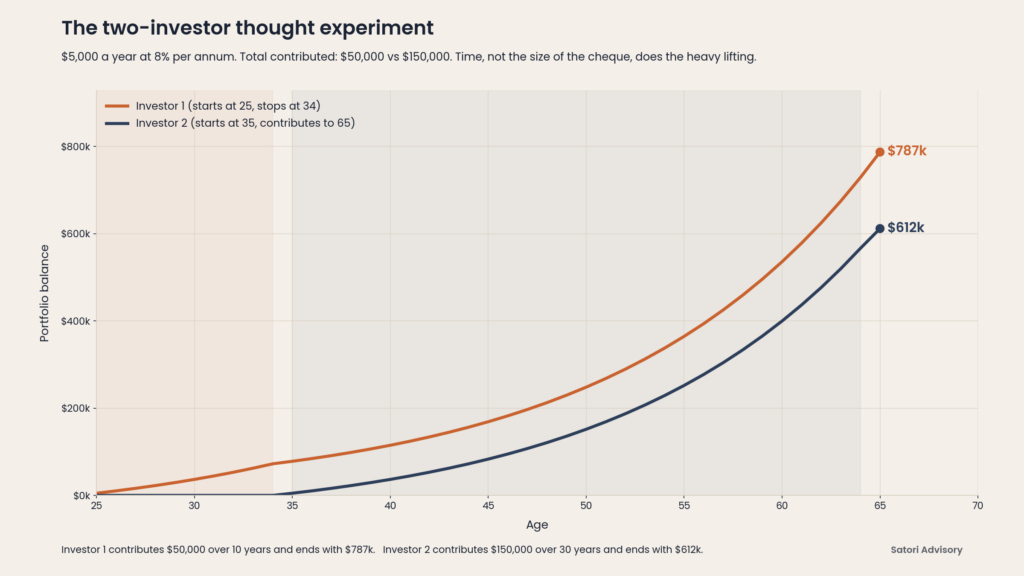

Picture two Australians. Same 8% annual return. Same retirement age of 65. Different starting age, different total contribution.

- Investor 1 starts at age 25 and puts in $5,000 every year for 10 consecutive years. After age 34, they stop. They never add another dollar. The balance is left to grow until age 65.

- Investor 2 starts at age 35 and puts in $5,000 every year for 30 consecutive years, all the way to age 65.

On paper this looks lopsided. Investor 1 contributes $50,000 in total. Investor 2 contributes $150,000. Three times the cash, three times the years of saving. Most people, asked to guess, will say Investor 2 wins.

Investor 2 does not win. Investor 1 wins, and not by a little.

At 8% per year, Investor 1 receives roughly 16 times their original $50,000 back. Investor 2 receives roughly 4 times their $150,000. The 25 year old who saved for one decade and stopped ends up with more money than the 35 year old who saved for three decades. They hit $1 million by age 68.

Read that again. An extra $175,000 of final wealth, with $100,000 less actually invested.

The reason is simple, and it is the entire point. Investor 1 gave their money 40 years of compounding. Investor 2 gave their money 30 years. Those 10 extra years are not a small advantage. They are the advantage. Each year the snowball is bigger, and so each year of compounding adds more in absolute dollars than the year before.

This is also why the most powerful financial favour an Australian parent can do for their children is not to help them buy a first car. It is to help them start investing in their twenties, and to leave it alone.

What 30 years of Australian asset class returns actually look like

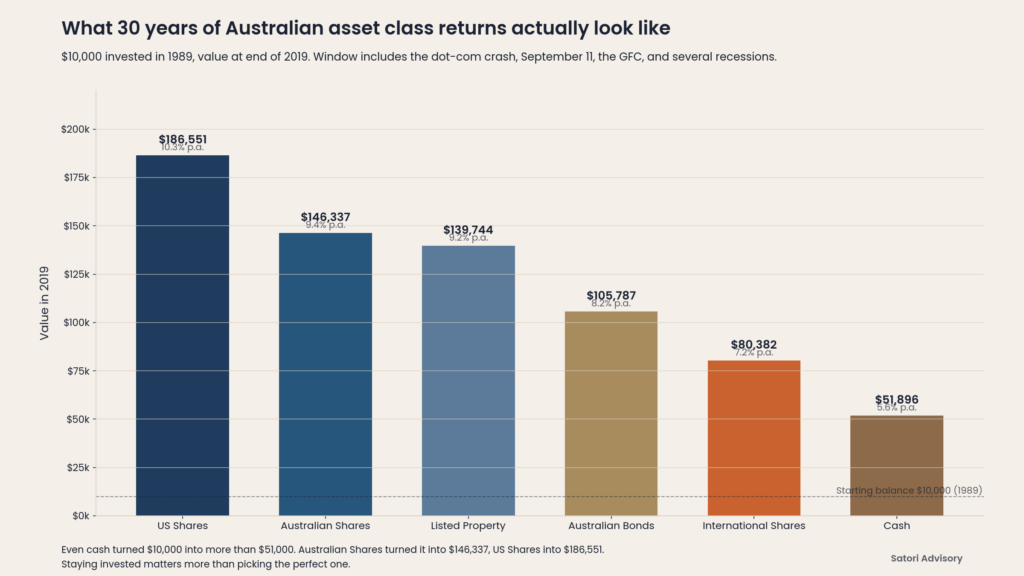

Compounding is not a theory. It is what shows up in the actual long-run data, including through stock market crashes, terror attacks, wars, multiple changes of government, and the Global Financial Crisis. Here is what $10,000 invested in 1989 had grown to by 2019, across the major asset classes available to an Australian investor.

| Asset class | Value of $10,000 in 2019 | Per annum return |

|---|---|---|

| Australian Shares | $146,337 | 9.4% |

| US Shares | $186,551 | 10.3% |

| Listed Property | $139,744 | 9.2% |

| Australian Bonds | $105,787 | 8.2% |

| International Shares | $80,382 | 7.2% |

| Cash | $51,896 | 5.6% |

A few things stand out. The lowest return on the page is Cash at 5.6% per annum. Even that turned $10,000 into more than $51,000, simply by being left alone. The highest, US Shares at 10.3% per annum, turned the same $10,000 into roughly $186,500. The gap between the bottom and the top is more than $134,000, on an identical starting cheque, over the same window.

Two practical points fall out of this. First, the asset class you choose matters, but staying in any of them for 30 years matters more than picking the perfect one. Second, the returns above are gross of tax and platform costs, so the order does not change but the size of the gap narrows. A diversified portfolio, sensibly structured, sits somewhere in the middle of this table and gets most of the benefit while smoothing out the ride.

Why time in the market beats timing the market

Most Australians who delay investing do not delay because the maths is unclear. They delay because the world is loud. There is always a reason to wait. A pending election, a frothy property market, a wobble in the US, a new recession warning, a recent crash that is still fresh.

The 30 year window above includes the dot-com crash, September 11, the Iraq war, the 2008 Global Financial Crisis, multiple federal governments, and several recessions. None of those events stopped Australian Shares from compounding at 9.4% per annum across the full window. The investor who tried to get out and back in at the right moments, in our experience, did worse than the investor who simply stayed in.

The trade-off is not ‘crash versus no crash’. The trade-off is ‘volatility you can see versus opportunity cost you cannot see’. Sitting in cash feels safe in the moment because the balance does not move. Across 30 years, that same cash position quietly cost $94,000 of foregone wealth on a $10,000 starting balance, compared with Australian Shares.

This is also why we generally do not market-time on behalf of clients. We design a portfolio that you can hold through the noise, then we hold it. Inside that, we rebalance, we use tax structures sensibly, and we keep enough liquidity that you never have to sell a quality asset at a bad time.

What this means for an Australian wealth builder today

If the maths is the easy part, the practical question is: what should you actually do with this idea in 2026?

The honest answer depends on which life stage you are in. For a 25 to 35 year old, the lesson is to start now, in something diversified and low cost, and to automate the contribution before lifestyle creep absorbs it. The Investor 1 outcome is not unreachable. It is just unreachable if you wait until your forties to start.

For a 35 to 55 year old, the lesson is to make every remaining year of compounding count. That usually means a higher contribution rate, a smarter use of super and structures, and a clear plan that you will not abandon at the next market wobble. The window is shorter, so the focus shifts to consistency and tax efficiency.

For a 55 plus year old, the lesson changes shape. Compounding is still working, but now it is working on the wealth you have already built. The job becomes preserving the base, drawing income sensibly, and making sure the structures behind your assets are not quietly leaking returns through tax, fees, or poorly diversified concentration risk.

What to do next

If this piece resonated, three questions are worth sitting with this week.

- Are you actually invested in growth assets right now, or are you holding more cash than your time horizon needs?

- If you have children or grandchildren in their twenties, what is the single most useful financial conversation you could have with them in the next 30 days?

- Is your current plan structured so that the compounding inside it survives the next market scare, or are you likely to interrupt it?

Behind the scenes our job is to make sure the maths above keeps working for you, in the right structures, with the right asset mix, across decades. If anything in this piece raised a question, please reach out.

How Satori Advisory works

At Satori Advisory we energise every part of your financial world. We integrate your tax, business, wealth and lending as a prosperity engine, aligned with what matters most to you. With a clear roadmap, informed by data and backed by decades of strategic experience, we simplify the complex. We do not offer pre-packaged solutions. We deliver tailored, end-to-end advice that reflects your reality and ambitions. You work directly with senior advisers who listen deeply, think boldly and act with purpose, supported by our trusted team and curated network of financial and business specialists, so you can realise your potential, powered by numbers.

Ready to talk?

If you would like a calm, no-pressure conversation about how to put the power of compound interest to work in your own plan, we would be glad to set one up.

Call 1300 925 081 or email [email protected].

Or book a complimentary 30-minute meeting with one of our senior advisers.

Frequently asked questions

What is the power of compound interest in simple terms?

Compound interest is interest earned on both your original investment and on the interest it has already produced. Each year the base grows, and each year the next year’s growth is calculated off a bigger base. Across decades, this snowball effect produces returns that look almost unrealistic compared with simple interest, which is why so much of long-term wealth comes from time in the market rather than from the size of any single contribution.

Did Albert Einstein actually call compound interest the eighth wonder of the world?

The ‘eighth wonder of the world’ line is commonly attributed to Albert Einstein, but it is widely regarded as apocryphal. There is no verified primary source where Einstein said or wrote it. The phrase is still useful as a memorable framing of the same underlying point: compounding produces results that feel disproportionate to the inputs, particularly across long time horizons.

How can a 25 year old who only saves for 10 years end up wealthier than a 35 year old who saves for 30 years?

At an 8% annual return, an investor who contributes $5,000 a year from age 25 to 34 (a total of $50,000) and then leaves the balance alone until age 65 typically ends up with more than an investor who contributes $5,000 a year from age 35 to 65 (a total of $150,000). The earlier investor’s money has 40 years of compounding, the later investor’s money has 30. Those 10 extra years are doing the heavy lifting, because each year of compounding adds more in absolute dollars than the one before.

What did $10,000 invested in Australian asset classes in 1989 grow to by 2019?

Across the 30 years to 2019 (historical reference), $10,000 grew to $146,337 in Australian Shares (9.4% per annum), $186,551 in US Shares (10.3%), $139,744 in Listed Property (9.2%), $105,787 in Australian Bonds (8.2%), $80,382 in International Shares (7.2%), and $51,896 in Cash (5.6%). The window included the dot-com crash, September 11, the Iraq war, the Global Financial Crisis, and several recessions, and the long-term compounding still held up.

Is it ever too late to start investing in Australia?

No. The honest framing is that it is rarely too early and almost never too late, but the levers change with age. In your twenties and thirties, time is the biggest lever. In your forties and fifties, contribution rate, structure, and tax efficiency become the biggest levers. From your late fifties onward, the focus shifts to preserving the base, drawing income sensibly, and not letting fees, tax, or concentration risk quietly leak your returns.

Please feel free to get in touch on 1300 925 081 or send an email to [email protected] if you’d like to book in a chat on the above or on other matters.